Break Free from Debt Chains: Discover the Power of Consolidation Loans Today!

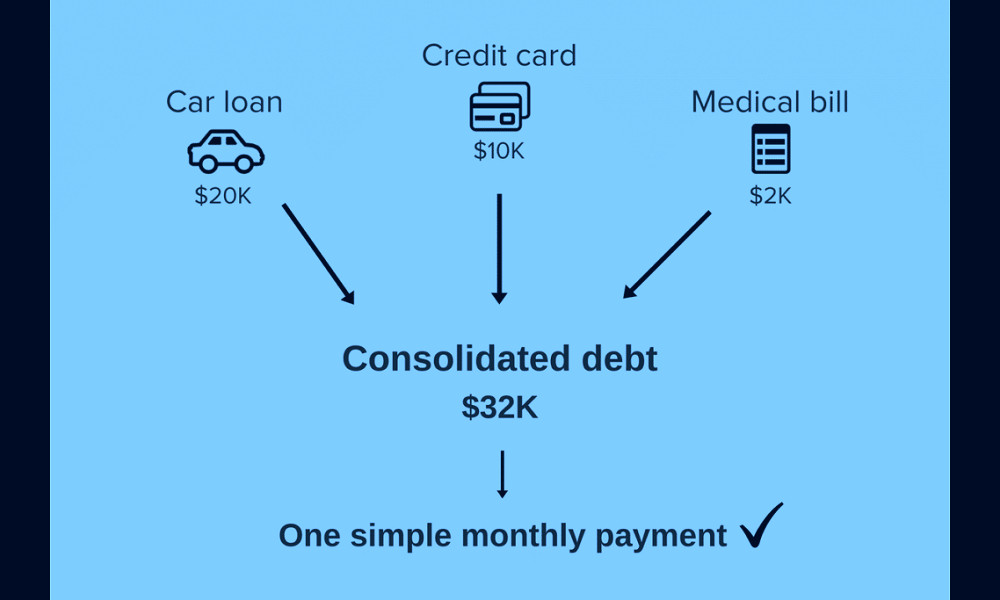

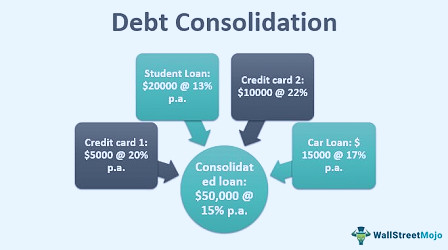

Debt consolidation loans are financial tools that allow you to combine multiple debts into one single loan. This means instead of managing various payments each month, you only need to make one. By merging high-interest debts into a lower-interest loan, you can often reduce your monthly payments and the total amount you owe over time. It's a smart strategy for those seeking to simplify their financial life and potentially save on interest costs.

| Type | Personal Loan |

| Purpose | Debt Consolidation |

| Loan Amount Range | Depending on the lending institution |

| Interest Rates | Depending on the lending institution, credit score, and loan amount |

| Loan Term | Varies by lender, typically 1-7 years |

| Repayment Options | Monthly |

| Secured or Unsecured | Typically Unsecured |

| Credit Score Requirement | Varies by lender |

| Fees | Origination fee, late fee, prepayment penalty (depending on the lender) |

| Approval Time | Varies by lender |

| Funds Disbursement Time | Varies by lender |

| Online Application | Available with most lenders |

| Customer Support | Varies by lender |

| Lender Reputation | Varies by lender |

| Eligibility | 18 years of age, valid bank account, proof of steady income, good credit score (varies by lender) |

| Additional Features | Some lenders offer financial education resources or tools to track your credit score |

| Loan Use | Pay off multiple debts with a single loan |

| Benefits | Lower interest rate, single monthly payment, improved credit score (over time) |

| Cons | Potential fees, could end up paying more in long term if not managed properly |

| Terms and Conditions | Varies by lender |

| Privacy Policy | Varies by lender. |

![4 Best Debt Consolidation Loans for Bad Credit [August 2023]](/img/debt-consolidation-loans.big.31.jpg)

Understanding Debt Consolidation

Debt consolidation is a financial strategy that combines multiple debts into a single loan. This tactic is often used by individuals who have high-interest debts and are looking to simplify their payments. The key advantage of debt consolidation loans is that they usually come with a lower interest rate than what you're currently paying, which can save you money in the long run. Read more

Assess Your Debt Situation

Before choosing a debt consolidation loan, it's essential to evaluate your current debt situation. This includes tallying up your total debt, understanding the interest rates you're paying, and determining your monthly payments. This baseline information will help you decide if consolidation is the right strategy for you. Read more

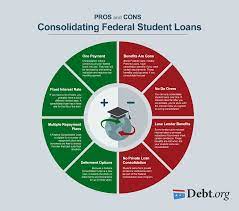

The Pros of Debt Consolidation Loans

Debt consolidation loans have several advantages. They simplify your payments by combining all your debts into one monthly payment. This can make it easier to manage your finances. Additionally, debt consolidation loans typically have lower interest rates than your current debts, which can save you money over time. Read more

The Cons of Debt Consolidation Loans

It's essential to be aware of potential downsides when considering a debt consolidation loan. These loans might extend your repayment period, meaning you could be in debt for a longer time. They also might have upfront costs or fees. You need to make sure that the benefits outweigh the potential drawbacks. Read more

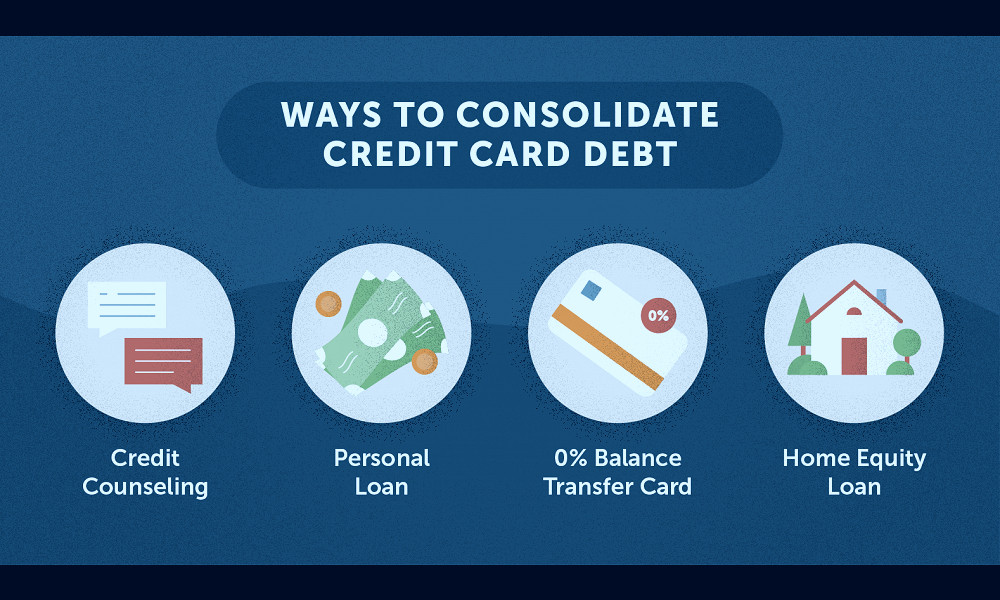

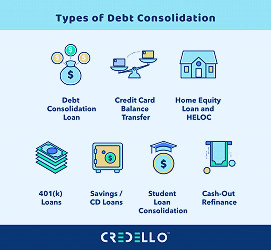

Types of Debt Consolidation Loans

It's worth noting that there are several types of debt consolidation loans. These include personal loans, home equity loans, and balance transfer credit cards. Each has its own pros and cons, and the best choice will depend on your personal financial situation. Read more

Comparing Debt Consolidation Loan Providers

Not all debt consolidation loan providers are created equal. It's crucial to compare interest rates, fees, loan terms, and customer reviews when choosing a provider. Online loan comparison tools can be a valuable resource in this process. Read more

Applying for a Debt Consolidation Loan

The application process for a debt consolidation loan typically involves providing your personal and financial information, including your income, employment status, and total debt. Lenders will also check your credit score to determine your eligibility and interest rate. Read more

Debt Consolidation and Your Credit Score

Initially, applying for a debt consolidation loan may slightly lower your credit score due to the hard inquiry on your credit report. However, over time, making consistent, on-time payments can help improve your credit score. Read more

Alternatives to Debt Consolidation Loans

If a debt consolidation loan isn't right for you, there are other options to consider. These might include debt management plans, debt settlement, or in severe cases, bankruptcy. It's crucial to research and understand these alternatives before making a decision. Read more

Consult a Financial Advisor

Debt consolidation loans can be a useful tool for managing and reducing debt, but they aren't right for everyone. A financial advisor can help you assess your debt situation, explore all your options, and make the best decision for your financial future. Read more

Facts

1. Battle Against High-Interest Rates:Debt consolidation loans are your ultimate weapon to wage war on high-interest rates. With a single, lower-interest rate loan, you can simplify your payments and reduce the overall interest you pay. It's like slaying a many-headed beast with one swift stroke!

2. A Lifesaver for Multiple Debts:

Are you juggling multiple loans and credit cards? Debt consolidation brings them all under one roof, making it easier to manage. In essence, it's like having a personal finance superhero swooping in to save the day, rescuing you from the stress of multiple debts.

3. Credit Score Saver:

Did you know that debt consolidation loans can also act as your credit score's knight in shining armor? By consolidating your debts and making regular repayments, you can demonstrate responsible borrowing which may improve your credit score over time. It's like a financial fitness regime for your credit health.

4. The Power of Fixed Repayments:

With debt consolidation loans, you can enjoy the stability of fixed repayments. This means no more nasty surprises or fluctuating payment amounts. It's like your financial life suddenly becomes a calm sea after a storm.

5. No Collateral, No Problem:

Unlike secured loans, debt consolidation loans often don't require collateral. This means you don't have to risk your home or car to get one. It's like taking a big financial step without having to put your most prized possessions on the line.

6. Freedom from Debt Faster:

With a clear repayment schedule and lower interest rates, you can potentially become debt-free faster with a debt consolidation loan. It's like finding a secret shortcut on your road to financial freedom.

7. The Beauty of Simplicity:

Managing multiple debts can be like trying to solve a complicated puzzle. A debt consolidation loan simplifies this process, turning it into a straightforward task. It's like swapping a Rubik's cube for a jigsaw puzzle.

8. A Solution Tailored for You:

Debt consolidation loans can be tailored to suit your individual financial situation. It's like having a bespoke suit crafted, but for your finances. Ensuring a comfortable fit for your budget and lifestyle.

9. The Ultimate Stress-Reducer:

Consolidating your debts into one manageable payment can significantly reduce your financial stress. It's like a deep breath of fresh air amidst the chaos of juggling multiple repayments.

10. The Path to Better Money Habits:

A debt consolidation loan can also act as a catalyst for better money habits. With clearer visibility of your debts and repayments, you can develop more effective budgeting and money management skills. It's like a stepping stone on your journey towards financial wisdom.

Read more

Does Debt Consolidation Hurt Your Credit?

Does Debt Consolidation Hurt Your Credit? What Is a Debt Consolidation Loan? - The Kansas City Star

What Is a Debt Consolidation Loan? - The Kansas City Star Debt Consolidation Loans: How to Reduce Your Personal Debt

Debt Consolidation Loans: How to Reduce Your Personal Debt What is Debt Consolidation & How to Do It | Credello

What is Debt Consolidation & How to Do It | Credello What is Debt Consolidation & How to Do It | Credello

What is Debt Consolidation & How to Do It | Credello Debt Consolidation - U of I Community Credit Union

Debt Consolidation - U of I Community Credit Union Debt Consolidation Loan - SafeAmerica Credit Union

Debt Consolidation Loan - SafeAmerica Credit Union Pros and Cons of Student Loan Consolidation for Federal Loans

Pros and Cons of Student Loan Consolidation for Federal Loans Debt Consolidation - What Is It, Pros And Cons, How To Get?

Debt Consolidation - What Is It, Pros And Cons, How To Get? Personal Loans for Debt Consolidation: What's The Average Amount?

Personal Loans for Debt Consolidation: What's The Average Amount? Why you should get a debt consolidation loan now - CBS News

Why you should get a debt consolidation loan now - CBS News What is Debt Consolidation & How to Do It | Credello

What is Debt Consolidation & How to Do It | Credello Best Debt Consolidation Loans 2023 - Find Rates & Apply Online - Intuit Credit Karma

Best Debt Consolidation Loans 2023 - Find Rates & Apply Online - Intuit Credit Karma Debt Consolidation Meaning, Definitions, & Facts | Americor

Debt Consolidation Meaning, Definitions, & Facts | Americor 5 Best Debt Consolidation Loans for Bad Credit (Aug. 2023) | BadCredit.org

5 Best Debt Consolidation Loans for Bad Credit (Aug. 2023) | BadCredit.org![11 Best Debt Consolidation Loans of 2023 [updated monthly]](/static/debt consolidation loans/16.thumb.jpg) 11 Best Debt Consolidation Loans of 2023 [updated monthly]

11 Best Debt Consolidation Loans of 2023 [updated monthly]![Debt Consolidation Loan vs Debt Management Program [Infographic]](/static/debt consolidation loans/17.thumb.jpg) Debt Consolidation Loan vs Debt Management Program [Infographic]

Debt Consolidation Loan vs Debt Management Program [Infographic] Is Debt Consolidation a Good Idea for You? - LendingPoint

Is Debt Consolidation a Good Idea for You? - LendingPoint Debt Consolidation Loans: What You Need to Know | Lexington Law

Debt Consolidation Loans: What You Need to Know | Lexington Law Debt Consolidation Loan Solutions When Your Application Was Declined

Debt Consolidation Loan Solutions When Your Application Was Declined