Master Your Golden Years: A Comprehensive Guide to Effective Retirement Planning

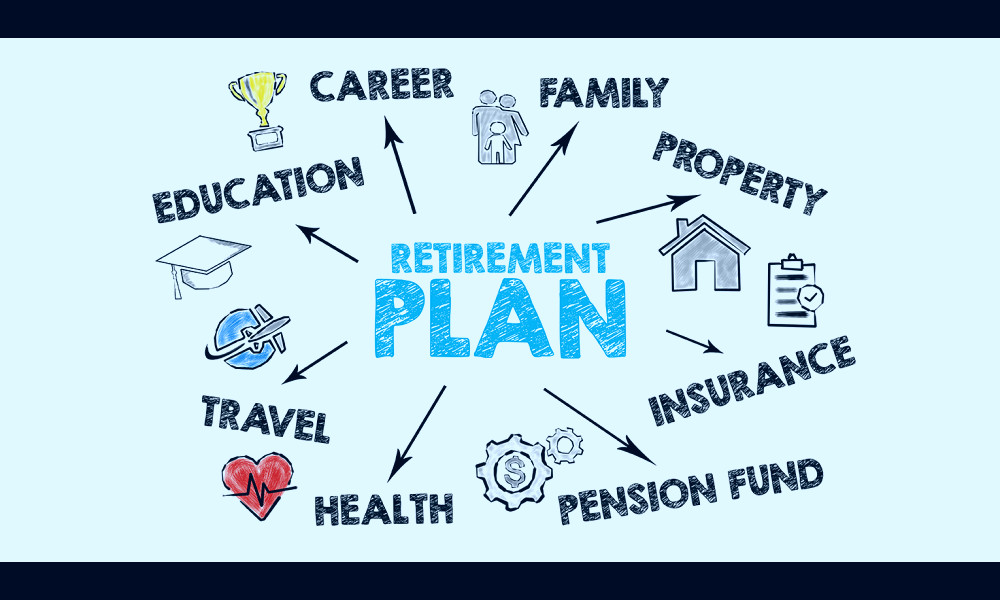

Retirement Planning is a comprehensive approach to ensure financial security and stability during the twilight years of life. It involves a systematic strategy of savings, investments, and asset management, tailored to accumulate sufficient funds for post-retirement life. The goal is to maintain a comfortable lifestyle, cover healthcare expenses and leave a financial legacy, without being reliant on any external income source. It is not a one-time event but a lifelong process that requires regular review and adjustments.

| Type of Service | Retirement Planning |

| Service Provider | Unknown |

| Service Description | A process of determining retirement income goals and the actions necessary to achieve those goals. |

| Consultation Type | Face-to-face, Online, Phone |

| Investment Strategies | Diversification, Asset Allocation, Risk Management |

| Retirement Goals | Financial Independence, Travel, Homeownership, Healthcare Expenses |

| Retirement Age | Customizable |

| Investment Options | Stocks, Bonds, Mutual Funds, ETFs, Real-estate, Annuities |

| Tax Considerations | IRA, 401(k), Roth IRA, Tax implications on withdrawals |

| Social Security Benefits | Estimation and Optimization |

| Pension Handling | Lump sum or Annuity |

| Inflation Considerations | Yes |

| Risk Tolerance | Low, Medium, High |

| Expected Return on Investment | Variable |

| Cost | Varies by provider and plan |

| Additional Services | Estate Planning, Tax Planning, Insurance Planning. |

| Customer Support | Call, Email, Live Chat |

| Note | The exact parameters might vary depending on the retirement planning service provider. |

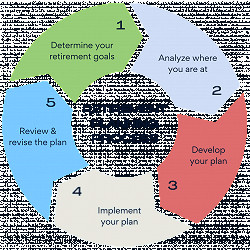

Understanding Retirement Planning

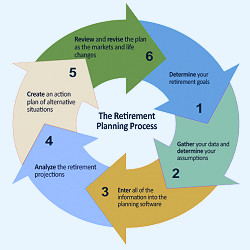

Retirement planning refers to the process of determining retirement income goals and the actions necessary to achieve these goals. It involves evaluating your current financial standing and creating an accumulation strategy that will help to ensure a desired retirement lifestyle. This planning process is multi-faceted and encompasses elements such as income, expenses, investments, and risk tolerance. Read more

The Importance of Retirement Planning

With the decrease in traditional pension plans and uncertainty surrounding social security benefits, it's important for individuals to take control of their financial future. A well-executed retirement plan provides for financial independence and can help to mitigate the risks associated with outliving your assets. Read more

Retirement Planning Strategies

Retirement strategies may include saving money in a retirement account like a 401(k) or IRA, investing in the stock market, real estate, or other avenues, and possibly purchasing an annuity for guaranteed income. The best strategy will depend on your individual circumstances, including your age, income, risk tolerance, and retirement goals. Read more

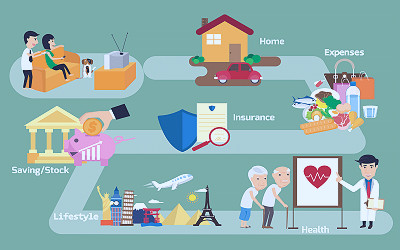

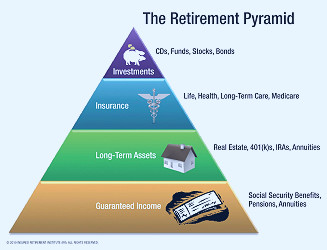

Retirement Income Sources

A major aspect of retirement planning involves understanding potential sources of retirement income. These typically include social security, pensions, personal savings, and investments. The combination of these income streams will determine your financial stability in retirement. Read more

Investment Management in Retirement Planning

Proper investment management is crucial to a successful retirement plan. This involves asset allocation, risk management, and ensuring your portfolio is diversified to withstand market fluctuations. Working with a financial advisor can help you navigate these complexities. Read more

Retirement Savings Vehicles

Choosing the right retirement savings vehicle can have a significant impact on your financial future. Options may include employer-sponsored plans like 401(k)s or 403(b)s, individual retirement accounts (IRAs), and other savings accounts. Each offers different advantages in terms of tax benefits, contribution limits, and withdrawal rules. Read more

The Role of Insurance in Retirement Planning

Insurance products like long-term care insurance, life insurance, and annuity contracts can play a key role in your retirement plan. They can provide financial protection against unforeseen events and can offer an additional source of retirement income. Read more

Factors Affecting Retirement Planning

Numerous factors can impact your retirement plan. These include your projected lifespan, health, inflation, and economic conditions. It's important to consider these factors and adjust your plan as necessary to ensure a comfortable retirement. Read more

Estate Planning and Retirement

Estate planning is an important component of retirement planning. This involves determining how your assets will be distributed upon your death. Proper estate planning can help to reduce taxes and ensure your wishes are carried out. Read more

Professional Help for Retirement Planning

Navigating the complexities of retirement planning can be challenging. Working with a financial planner or advisor who specializes in retirement planning can provide valuable guidance. They can help you create a comprehensive plan that considers all aspects of your financial situation and aligns with your retirement goals. Read more

Facts

1. The Early Bird Catches the Worm: Did you know that starting your retirement planning early can exponentially increase your savings? Thanks to the power of compound interest, every dollar you put aside today could turn into many more by the time you retire. The earlier you start, the more time your money has to grow.2. It's Not Only About Saving: While saving is a crucial part of retirement planning, it's not the only factor. Smart investments can help build your retirement fund faster. Diversifying your portfolio with a mix of stocks, bonds, and mutual funds can potentially yield higher returns over the long term.

3. Retirement Planning Is Not One-size-fits-all: Everyone's retirement needs and goals are different. Some people dream of traveling the world, while others look forward to a quiet life in the countryside. A good retirement plan takes into account your personal goals, life expectancy, and health, among other factors.

4. Living Longer Means Saving More: With advances in healthcare and lifestyle changes, people are living longer than ever. This means you could spend more years in retirement, and hence, you'll need a bigger retirement fund. It's important to consider longevity when planning for retirement.

5. Inflation Is a Silent Enemy: While it's not as noticeable as a stock market crash, inflation can significantly erode your retirement savings. It's important to factor in inflation when calculating how much you'll need for retirement.

6. Social Security Is Not Enough: Social Security can provide a safety net, but it's not enough to rely on solely for retirement. On average, Social Security benefits replace about 40% of pre-retirement income, which is why personal savings and investments play a crucial role in retirement planning.

7. Tax-Advantaged Retirement Accounts: Taking advantage of tax-advantaged retirement accounts like 401(k)s and IRAs can help you save more for retirement. These accounts offer tax benefits that can significantly boost your retirement savings over time.

8. The Power of Annuities: Annuities can provide a steady stream of income in retirement. They're insurance products that you pay for upfront, and then they pay you back over time, often for the rest of your life. They can be a powerful tool in retirement planning.

9. The Importance of Estate Planning: Estate planning is an often overlooked part of retirement planning. A good estate plan ensures that your assets are distributed according to your wishes after your death. It can also help minimize taxes and avoid probate.

10. Retirement Planning Is Ever-evolving: Retirement planning is not a set-it-and-forget-it process. It's important to regularly review and adjust your plan based on changes in your life, market conditions, and financial goals.

Read more

Retirement Planning: How to Plan Your Financial Journey | The Motley Fool

Retirement Planning: How to Plan Your Financial Journey | The Motley Fool Retirement Planning 101

Retirement Planning 101 Retirement Plans - Types Of Accounts and Their Differences

Retirement Plans - Types Of Accounts and Their Differences 5 Important Steps to Retirement Planning - Meld Financial

5 Important Steps to Retirement Planning - Meld Financial Retirement Planning - Step By Step - First Point Wealth Management

Retirement Planning - Step By Step - First Point Wealth Management A More Holistic Approach to Retirement Planning | myLifeSite

A More Holistic Approach to Retirement Planning | myLifeSite Myth busting three common retirement planning beliefs - Prenger and Profitt

Myth busting three common retirement planning beliefs - Prenger and Profitt Important & Decisions for Each Phase of Retirement Planning

Important & Decisions for Each Phase of Retirement Planning Thinking about retirement? Retirement Planner in Columbia SC

Thinking about retirement? Retirement Planner in Columbia SC Simple Habits That Can Bolster Your Retirement Plans - WiserAdvisor - Blog

Simple Habits That Can Bolster Your Retirement Plans - WiserAdvisor - Blog Retirement Planning :

Retirement Planning : Retirement Planning - MKG Insurance Agency

Retirement Planning - MKG Insurance Agency Retirement Planning | Human Resources

Retirement Planning | Human Resources Retirement Planning checklist - WiserAdvisor - Blog

Retirement Planning checklist - WiserAdvisor - Blog 9 Reasons Why Retirement Planning is Important

9 Reasons Why Retirement Planning is Important Personal Capital Retirement Planner - Happy FinServ

Personal Capital Retirement Planner - Happy FinServ Planning for your Retirement | Department of Insurance, SC - Official Website

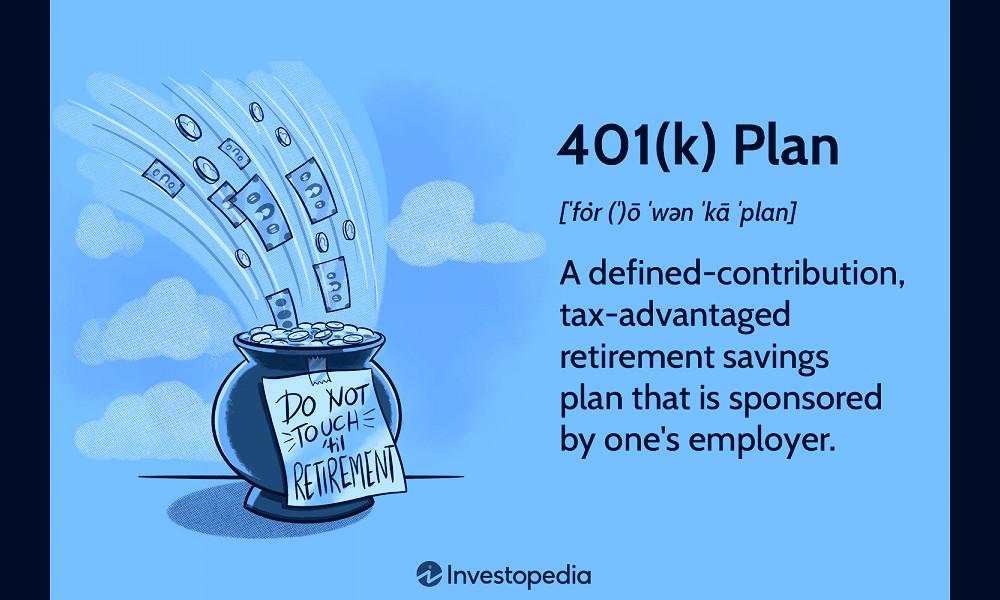

Planning for your Retirement | Department of Insurance, SC - Official Website What Is a 401(k) and How Does It Work?

What Is a 401(k) and How Does It Work? Why should you want professional help with your financial planning? - Rowling & Associates

Why should you want professional help with your financial planning? - Rowling & Associates Pandemic Heightens Need for Retirement Planning

Pandemic Heightens Need for Retirement Planning