Unlock Financial Freedom: Choosing the Right Debt Consolidation Program for You!

Debt consolidation programs are financial solutions designed to help individuals manage their multiple debts more effectively. This service consolidates various debts into one manageable monthly payment, often with a lower interest rate. It simplifies the debt repayment process, potentially saves money on interest, and provides an achievable pathway towards financial freedom. Ideal for those feeling overwhelmed by numerous debts like credit cards, student loans, or medical bills, a debt consolidation program provides a structured plan to regain control over one's finances.

| Program Name | Debt Consolidation Program |

| Type | Debt relief service |

| Service Provided | Consolidation of multiple debts into one single payment |

| Eligibility Criteria | Having multiple unsecured debts, ability to make monthly program payments |

| Interest Rate | Varies based on lenders and individual credit score |

| Monthly Payment | Determined based on total debt amount and program duration |

| Program Duration | Varies, typically 2-5 years |

| Fees | May include one-time setup fee and monthly service fee |

| Impact on Credit Score | May initially lower, but can improve over time with consistent on-time payments |

| Counseling Services | Often included, providing education on budgeting and financial management |

| Additional Services | May include negotiations with creditors to lower interest rates or waive fees |

| Guarantee | No guarantee, success depends on individual's adherence to program and financial circumstances |

| Provider | Various financial institutions and credit counseling agencies |

| Legal Protection | May provide some protection from creditor lawsuits and debt collection activity |

| Debt Types Covered | Typically unsecured debts such as credit card debt, personal loans, medical bills |

| Restrictions | May not include secured debts like mortgages or auto loans, or federal student loans in some cases |

| Requirements | Regular income, commitment to not accruing additional debt during program |

| Benefits | Single monthly payment, potential interest rate reduction, education and support, potential for faster debt payoff |

| Risks | Potential negative impact on credit score, potential fees, requirement to not accrue additional debt during program. |

![Debt Consolidation Guide: How Does It Work? [July 2023]](/img/debt-consolidation-programs.big.4.jpg)

![4 Best Debt Consolidation Loans for Bad Credit [August 2023]](/img/debt-consolidation-programs.big.12.jpg)

Understanding Debt Consolidation

Debt consolidation is a strategy that combines multiple debts into a single, manageable payment. It involves taking out a new loan or credit card to pay off existing debts, thereby simplifying the repayment process and potentially saving money on interest. Read more

Benefits of Debt Consolidation

One of the primary benefits of debt consolidation is its simplicity. Instead of managing multiple payments each month, borrowers can focus on a single payment. Additionally, debt consolidation often comes with lower interest rates, which can save considerable amounts of money over time. Read more

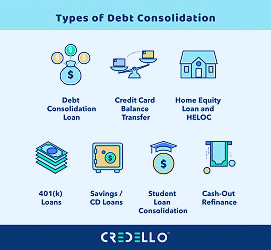

Types of Debt Consolidation Programs

Several types of debt consolidation programs are available, including personal loans, balance transfer credit cards, and home equity loans. The right choice for you will depend on your personal financial situation, credit score, and the amount of debt you have. Read more

Understanding Interest Rates

A key factor in choosing a debt consolidation program is the interest rate. Lower interest rates mean lower monthly payments and less money paid over the life of the loan. It's essential to compare interest rates across different programs to ensure you're getting the best deal. Read more

Checking Credit Scores

Your credit score is a critical factor in determining which debt consolidation programs you're eligible for. Higher credit scores usually result in better interest rates, so it's worth checking your score and taking steps to improve it if necessary before applying for debt consolidation. Read more

Repayment Terms

When considering a debt consolidation program, it's crucial to understand the repayment terms. These terms outline how long you'll be making payments and what happens if you miss a payment. Always read the fine print to avoid any surprises down the line. Read more

Evaluating Fees

Some debt consolidation programs come with fees, such as origination fees or prepayment penalties. It's important to factor these into your decision-making process to ensure you're choosing the most cost-effective option. Read more

Impact on Credit Score

Debt consolidation can have a positive or negative impact on your credit score, depending on how you manage it. Making regular payments on time can improve your score, but missing payments can harm it. Understanding this impact can help you make an informed decision. Read more

Seeking Professional Advice

If you're unsure about which debt consolidation program to choose, it may be beneficial to seek professional financial advice. Financial advisors can provide personalized advice based on your unique circumstances, making it easier to choose the right program. Read more

Conclusion

Debt consolidation can be a helpful tool for managing and reducing debt. However, it's essential to carefully consider your options and understand the potential impacts before making a decision. With careful planning and consideration, debt consolidation can be a powerful tool for financial stability. Read more

Facts

1. The Purpose: Debt consolidation programs are designed to help you get out of debt faster. By consolidating your debts into one monthly payment, you can save on interest rates and stop juggling multiple bills.2. Convenience: Instead of having to remember multiple due dates for various loans or credit card bills, debt consolidation programs allow you to make one single payment each month. This makes managing your finances significantly easier.

3. Lower Interest Rates: One of the major benefits of debt consolidation programs is the potential for lower interest rates. This can save you a substantial amount of money in the long run.

4. Improving Credit Score: By making regular, on-time payments through a debt consolidation program, you have the opportunity to improve your credit score over time.

5. Financial Education: Many debt consolidation programs also offer financial education resources and counseling. This can help you gain a better understanding of your finances and avoid falling into debt in the future.

6. Pay Off Debt Faster: With lower interest rates and a single monthly payment, you’re likely to pay off your debt faster than if you continued to make multiple payments with higher interest rates.

7. Reduced Stress: Financial stress can take a toll on your mental and physical health. By consolidating your debts, you can reduce your financial stress and focus on other areas of your life.

8. Customized Plans: Debt consolidation programs are not one-size-fits-all. Most providers will work with you to create a repayment plan that fits your budget and financial goals.

9. Beware of Scams: While there are many reputable debt consolidation programs out there, it’s important to be aware of potential scams. Always do your research and choose a credible provider.

10. Long-Term Solution: Debt consolidation programs can be a powerful tool for overcoming financial struggles. However, it’s important to remember that they are not a quick fix, but rather a long-term solution that requires commitment and discipline.

Read more

![Best Debt Consolidation Loan Companies and Programs [year]](/static/debt consolidation programs/1.thumb.jpg) Best Debt Consolidation Loan Companies and Programs [year]

Best Debt Consolidation Loan Companies and Programs [year] What is Debt Consolidation & How to Do It | Credello

What is Debt Consolidation & How to Do It | Credello![Debt Consolidation Loan vs Debt Management Program [Infographic]](/static/debt consolidation programs/3.thumb.jpg) Debt Consolidation Loan vs Debt Management Program [Infographic]

Debt Consolidation Loan vs Debt Management Program [Infographic]![Debt Consolidation Guide: How Does It Work? [July 2023]](/static/debt consolidation programs/4.thumb.jpg) Debt Consolidation Guide: How Does It Work? [July 2023]

Debt Consolidation Guide: How Does It Work? [July 2023] Debt Relief Programs: Explore Your Options and Make a Plan

Debt Relief Programs: Explore Your Options and Make a Plan Debt Consolidation Loans: How to Reduce Your Personal Debt

Debt Consolidation Loans: How to Reduce Your Personal Debt Get debt help by with the right debt management plan

Get debt help by with the right debt management plan What is Debt Consolidation & How to Do It | Credello

What is Debt Consolidation & How to Do It | Credello Debt Consolidation vs. Credit Counseling | InCharge.org

Debt Consolidation vs. Credit Counseling | InCharge.org 5 Best Debt Relief Companies & Debt Settlement Programs of 2023

5 Best Debt Relief Companies & Debt Settlement Programs of 2023 Debt Consolidation - What Is It, Pros And Cons, How To Get?

Debt Consolidation - What Is It, Pros And Cons, How To Get?![4 Best Debt Consolidation Loans for Bad Credit [August 2023]](/static/debt consolidation programs/12.thumb.jpg) 4 Best Debt Consolidation Loans for Bad Credit [August 2023]

4 Best Debt Consolidation Loans for Bad Credit [August 2023] Personal Loans for Debt Consolidation: What's The Average Amount?

Personal Loans for Debt Consolidation: What's The Average Amount? Pros and Cons of Debt Consolidation | Bankrate

Pros and Cons of Debt Consolidation | Bankrate What is Debt Consolidation and How Can It Help You? – Debt.com

What is Debt Consolidation and How Can It Help You? – Debt.com 5 Best Debt Relief Companies & Debt Settlement Programs of 2023

5 Best Debt Relief Companies & Debt Settlement Programs of 2023 Best Debt Consolidation Loans 2023 - Find Rates & Apply Online - Intuit Credit Karma

Best Debt Consolidation Loans 2023 - Find Rates & Apply Online - Intuit Credit Karma Debt Consolidation Companies BBB Accredited

Debt Consolidation Companies BBB Accredited Debt Consolidation vs Debt Management: Which is Best?

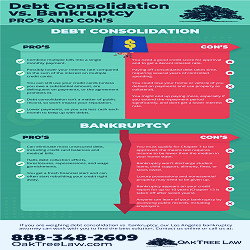

Debt Consolidation vs Debt Management: Which is Best? Debt Consolidation vs. Bankruptcy Pro's and Con's - Oaktree Law

Debt Consolidation vs. Bankruptcy Pro's and Con's - Oaktree Law