Exploring the Benefits and Features of BCC Personal Loans

BCC Personal Loans offer a wide range of flexible financing solutions tailored to meet your individual needs. Whether you're planning a big purchase, consolidating debt, or just need extra cash, BCC personal loans provide you with quick and easy access to funds. Enjoy competitive interest rates, fast approvals, and a convenient application process. With BCC Personal Loans, achieving your financial goals is made simpler.

Understanding Personal Loans

Personal loans are a type of unsecured loan issued by banks, credit unions, and other financial institutions. These loans can be used for a wide variety of purposes, from consolidating high-interest credit card debt to financing a large purchase or life event. Read more

The Role of BCC in Personal Loans

BCC, or Bank Credit Counsellor, plays a significant role in personal loans. They offer various types of loans, including personal loans, to their customers. They are known for their competitive interest rates and flexible repayment terms. Read more

BCC Personal Loans Features

BCC provides personal loans with no collateral required. This means that you do not have to put up any assets as security for the loan. Their loan amounts range from small to large, depending on the borrower's requirements and creditworthiness. Read more

Interest Rates on BCC Personal Loans

BCC offers competitive interest rates on their personal loans. The rate you receive will depend on various factors, including your credit score, income, and the loan amount and term. Read more

Applying for a BCC Personal Loan

BCC makes it easy to apply for a personal loan. You can apply online, over the phone, or in-person at a BCC branch. They require some basic financial and personal information, and the process is typically quick and straightforward. Read more

Repaying a BCC Personal Loan

BCC offers flexible repayment options for their personal loans. You can choose from various repayment periods, and there are no penalties for early repayment. This allows you to pay off your loan sooner and save on interest costs if you are able. Read more

The Impact on Your Credit Score

Like any other form of credit, a personal loan from BCC will have an impact on your credit score. If you make your payments on time and in full, it can help to boost your credit score. However, missed or late payments can negatively impact your score. Read more

BCC Personal Loan Eligibility

BCC has certain eligibility criteria for their personal loans. Generally, you need to be at least 18 years old, have a steady source of income, and have a good credit history. The specific requirements may vary depending on the loan amount and term. Read more

Customer Service at BCC

BCC is known for its excellent customer service. Their team is available to answer any questions you may have about personal loans, and they strive to make the process as easy and stress-free as possible. Read more

The Bottom Line on BCC Personal Loans

A personal loan from BCC can be a great option if you need funds for a large purchase or to consolidate high-interest debt. Their competitive interest rates, flexible repayment options, and excellent customer service make them a top choice for personal loans. Read more

Read more

BCBCC ADVANTAGE LOANS - BCBCC

BCBCC ADVANTAGE LOANS - BCBCC BCU | Personal Loans & Line of Credit

BCU | Personal Loans & Line of Credit BCC Carate Brianza - Crunchbase Company Profile & Funding

BCC Carate Brianza - Crunchbase Company Profile & Funding 7 Personal Loan Mistakes to Avoid

7 Personal Loan Mistakes to Avoid Best Personal Loans of July 2023: Compare Options

Best Personal Loans of July 2023: Compare Options BCC Credit Corporation | Mandaluyong

BCC Credit Corporation | Mandaluyong Payday Loans With a Personal Touch

Payday Loans With a Personal Touch Home - Bronx Community College – Bronx Community College

Home - Bronx Community College – Bronx Community College PersonalLoans.com Review (2023) – Personal Loans Up to $35k

PersonalLoans.com Review (2023) – Personal Loans Up to $35k The Best Credit Card of 2018 | Money

The Best Credit Card of 2018 | Money Shareholder Loans 2022 - YouTube

Shareholder Loans 2022 - YouTube Barthelemy Commercial Capital – A Lending and Business Consulting Firm

Barthelemy Commercial Capital – A Lending and Business Consulting Firm BCC Resources | Byram NJ

BCC Resources | Byram NJ Bcc Consultancy in Jalaram Chowk,Rajkot - Best Accountants in Rajkot - Justdial

Bcc Consultancy in Jalaram Chowk,Rajkot - Best Accountants in Rajkot - Justdial Business Credit Consulting

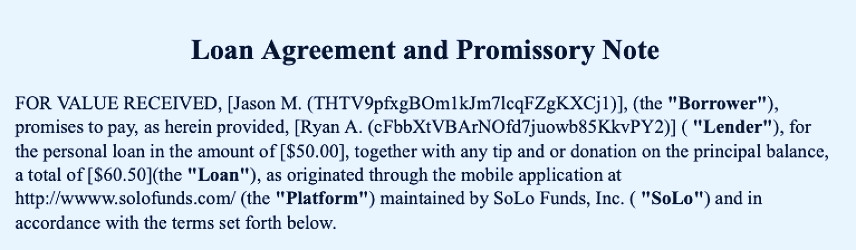

Business Credit Consulting Tips' & 'Donations' Can Reach 1,916% APR on Small Loans

Tips' & 'Donations' Can Reach 1,916% APR on Small Loans Payday Loans | Personal Loans | Line of Credit

Payday Loans | Personal Loans | Line of Credit Personal Loan - Balaji Corploan Consultants Pvt Ltd

Personal Loan - Balaji Corploan Consultants Pvt Ltd Sallie Mae Loans for Burlington County College Students | Uloop

Sallie Mae Loans for Burlington County College Students | Uloop Barthelemy Commercial Capital – A Lending and Business Consulting Firm

Barthelemy Commercial Capital – A Lending and Business Consulting Firm